Wall Street analysts have one job: predict where companies’ earnings are going in the coming quarter. Sounds simple enough, except said suits aren’t so good at it!

For the most recent earnings season, these forecasting fruit flies buzzed around modeling 12% earnings growth for the quarter. The S&P 500’s companies showed 27% profit growth–more than double what the “experts” predicted in their spreadsheets. They were way off.

So what does it mean when earnings come in at more than double the forecast? It means these companies have plenty of room–and reason–to hand more of that cash back to us. And that matters because over the long run stock prices follow their dividends.

We call this the dividend magnet: a stock’s payout tends to pull its price along with it. When a company cuts its dividend, the stock tanks–that’s the bad scenario. When a company raises its dividend, even at a yearly clip, its price moves at that same rate.

Buy in before the raise, and we lock in a fatter yield. Wait, and the market prices it away.

Which is why I’m watching eight stocks that have raised their payouts by as much as 77% over the past year. Historically these firms declare their raises during the summer months. This is the season to front run.

The “Hidden” Yielders

The most powerful dividend raisers often come from stocks that many investors overlook because of their thin headline yields. But if the raises continue at a frenetic pace, today’s fractional yields can be tomorrow’s fat paychecks.

Here’s a quick rundown of these mighty mini-payers:

- Argan (AGX, 0.3% dividend yield): This construction engineering firm sat on a flat dividend for years–then started hiking in 2023. The payout has doubled in just three years, including a 33.3% boost last year, following an explosion in the bottom line that’s expected to continue this fiscal year and next. Expected dividend announcement: Mid-September

- Chemed (CHE, 0.5% dividend yield): This bizarre holding company is held up by two major businesses: Roto-Rooter (the plumbing and drain cleaning service) and Vitas Healthcare (a large hospice and palliative care provider). Chemed has been raising its dividend without interruption for the better part of two decades, and it’s still hiking at a rapid clip–it has more than doubled its payout over the past five years and upped the ante by 20% in 2025 despite a pullback in profits. This year and next, the pros expect profits to rebound by double digits. Expected dividend announcement: Early August

- Howmet Aerospace (HWM, 0.2% dividend yield): Earlier this year, this engineered-products maker looked poised to make another semiannual dividend hike in late January–and then it didn’t. It’s not for lack of resources. Net income grew by 23% in 2025, and the pros see 33% growth this year and 20% in 2027. And HWM currently pays out less than 10% of 2026 earnings estimates. If Howmet were to adopt an annual dividend-raise schedule, the next hike would likely come sometime this summer–a year after it declared a 12-cent distribution that was 50% better YoY. Expected dividend announcement: Late July

- Comfort Systems (FIX, 0.2% dividend yield): This HVAC specialist has been growing like a weed–its net income nearly doubled in 2025, shares have rocketed 260% higher over the past year, and the current dividend is 77.7% higher than it was a year ago. FIX has raised its dividend multiple times per year since 2021 and has shelled out more cash for seven quarters straight. The pros expect no let-up in bottom-line growth, and with Comfort Systems paying out just 7% of this year’s earnings estimates, there’s no reason to expect any let-up in the distribution. Expected dividend announcement: Late July

- T-Mobile US (TMUS, 2.3% dividend yield): T-Mobile has evolved from a discount carrier into a true U.S. cellular powerhouse, going toe-to-toe with Verizon (VZ) and AT&T (T). Now it’s trying to mirror those telcos’ giant dividends. The company started its program in 2023 and has already pumped up that payout by another 57%. The 2%-plus yield, while bigger than the other companies mentioned, still isn’t much compared to AT&T and Verizon–but T-Mobile is rapidly closing the gap. Expected dividend announcement: Mid-September

Next up, our big dividends that could get even bigger:

Altria Group (MO)Dividend Yield: 5.7%2025 Increase: 4%Projected Q3 Distribution Announcement: Mid- to late August

Altria (MO) is best-known for its Philip Morris USA segment, which is responsible for the Marlboro brand and is far and away the company’s top revenue driver. But between increasingly stiff anti-smoking legislation and very real declines in volumes for years, some investors have given up the industry–and Altria–for dead.

But the company is putting increasing focus on its smokeless products, which include Copenhagen and Skoal smokeless tobacco, On! Oral nicotine pouches, NJOY e-vapor products and–through a joint venture with JT Group called Horizon Innovations–heated tobacco products. Nicotine pouches, for instance, might represent just 10% of the country’s nicotine volumes, but it’s a high-growth segment that’s expanding by about 25% annually. Altria’s hoping to capitalize on this with the national launch of its On! Oral brand and the recent release of higher-strength pouches.

MO has also been helped by its ability to command high prices for its products, as well as moderation in cigarette volume declines. And shares continue to benefit from the pull of its large-but-still growing dividend.

The Dividend Magnet’s Pull Is Finally Getting Some Business-Side Help of Late

Altria is a Dividend King, boasting more than five decades’ worth of uninterrupted dividend increases, so a dividend hike this summer seems like a sure thing. And it routinely makes its hike announcements in late August.

Virtus Investment Partners (VRTS)Dividend Yield: 6.7%2025 Increase: 7%Projected Q3 Distribution Announcement: Mid-August

Equity pariah Virtus Investment Partners (VRTS) is a specialized investment manager that provides mutual funds, exchange-traded funds (ETFs), closed-end funds (CEFs), insurance funds, separately managed accounts and more. Rather than a single large brand like Vanguard or Fidelity, Virtus is a partnership of numerous boutique investment advisers under a variety of flags: Voya, Ceredex, InfraCap, and more.

VRTS shares and dividend have largely been tethered to one another, which is what makes the past couple of years stand out.

Virtus and Its Payout Have Become Unglued

Virtus’ troubles aren’t nothing. It’s an actively managed outfit during a time when most major fund providers are racing each other into the low-fee basement. Several of its most important funds have struggled.

But put together both the past few years’ profits and what analysts expect to come, and we’re still looking at an upward trend. Meanwhile, VRTS has almost tripled its quarterly dividend in just five years, from 82 cents per share in 2021 to $2.40 today.

If Virtus keeps the pedal down on the distribution, shares might finally snap out of their funk. We’ll likely find out in mid-August, which is when the company has been announcing its annual raises.

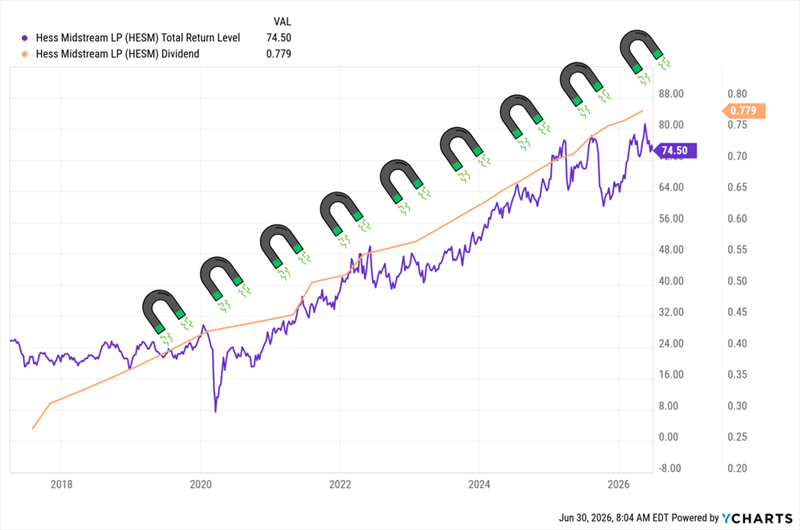

Hess Midstream LP (HESM)Dividend Yield: 8.3%2025 Increase: 10%Projected Q3 Distribution Announcement: Late July

Hess Midstream LP (HESM) is a master limited partnership (MLP) that owns, operates and develops a number of midstream energy assets, primarily located in the Williston Basin area of North Dakota. Those assets include natural gas and natural gas liquid (NGL) pipelines, gas processing facilities, crude oil terminals and gathering pipelines, water gathering pipelines, and more.

In early October 2025, I said HESM’s then-upcoming distribution announcement was a test. Chevron (CVX) closed on its acquisition of Hess (HES) in July, and it was an open question as to whether it would keep intact Hess Midstream’s streak of quarterly distribution hikes, which dates back to the payout’s start in 2017.

Good News: Chevron Let Hess Keep Cooking

Historically, HESM has delivered a drumbeat of 1%-3% quarter-over-quarter raises that have amounted to roughly 10% year-over-year growth. But the company recently pared back its full-year capex guidance and raised its free cash flow outlook, which could result in modestly thicker raises in the quarters to come (though it muddies the potential for growth). Whatever it chooses to do, it’s likely to come in late July.

5 Urgent Buys Set to Gain 15%+ Yearly… Potentially Forever? (Tickers Revealed Below)

Buying consistent dividend raisers is a time-tested blueprint for building lasting wealth. Boom or bust, rising dividends pull share prices up with them over the long haul.

Sometimes investing really is this simple!

The companies above are on my watch list right now, but they haven’t quite made my buy list. Topping them are five other stocks that are shelling out growing income streams AND annual returns of 15%, 17%, 21% and more.

Put simply: The average annualized yearly returns would be enough to double your investment every 5 years!

You don’t want to miss out on these always-rising dividends. Click here and I’ll walk you through these 5 robust dividend growers and give you a free Special Report revealing their names and tickers.